2024-01-24

When John Malone started to work, he sought a field that was:

He initially entered the cable business at Bell Labs, a subsidiary of AT&T, after earning his degree in operations research, which is essentially about minimizing "noise" and maximizing "output." He advised AT&T to reduce their debt and repurchase shares, but the board dismissed his recommendations. Consequently, he joined McKinsey.

At 29 years old, he began working at General Instruments, where he ran the Jerrold Cable Television division. Two years later, he had the option to work for either Warner Brothers or TCI. Despite facing a 60% pay cut, he chose TCI. Bob Magness founded TCI in 1956 and early on realized that he could avoid paying many taxes by taking on debt to build new systems and then depreciating them. He believed it was "better to pay interest than taxes." Magness's TCI became the fourth-largest cable company but carried debt equal to 17 times its revenues.

After a failed attempt to pay down the debt through an offering, they spent the next years fighting bankruptcy while meeting with bankers. Some other notable points include:

Note: There is a reverse relationship between investor returns and building a new headquarters (look at IAC, The New York Times).

TCI underpromised and overdelivered. When they emerged from their turmoil, Malone began implementing his strategy. He created a cycle: buy systems → lower programming costs → increase cash flow → get more leverage → buy systems → repeat.

In the cable business, revenue sharing with programmers is necessary, so Malone aimed to gain more negotiating power. Like many others, he did not want to focus on net income because it meant higher taxes. Instead, he prioritized internal growth and acquisitions with pretax cash flow.

"Ignoring EPS gave TCI an important early competitive advantage versus other public companies."

Malone also coined the term EBITDA, which is now common on Wall Street. Additionally, he bought more shares to reduce the risk of hostile takeovers.

In 1973, he started acquiring 482 companies until 1989, mostly funded by cash flow, debt, and equity offerings. Instead of focusing on large metropolitan franchises like his competitors, he concentrated on rural areas. He collaborated closely with entrepreneurs such as Ted Turner, John Sie, John Hendricks, and Bob Johnson to scout for new talent.

In 1990, the pace of acquisitions slowed down due to regulations on debt and the FCC tightening its regulations. In 1991, he began spinning off some parts, such as TCI's programming assets, into a new company called Liberty Media, in which he owned a significant stake. Subsequently, he continued to spin off parts.

In 1995, he delegated responsibility to a new management team. After a missed third quarter in 1996, he resumed leadership, reducing headcount, halting all orders for capital equipment, and renegotiating programming contracts. In the following years, he sold the spun-off businesses for a total of $33 billion. In the '90s, he began negotiations with AT&T to sell TCI due to his rationale indicating that the cable landscape would slow down.

"He turned the board of AT&T upside down, shook every nickel from their pockets, and returned them to their board seats." He wanted 12 times EBITDA. In 1999, he sold but still held Liberty Media.

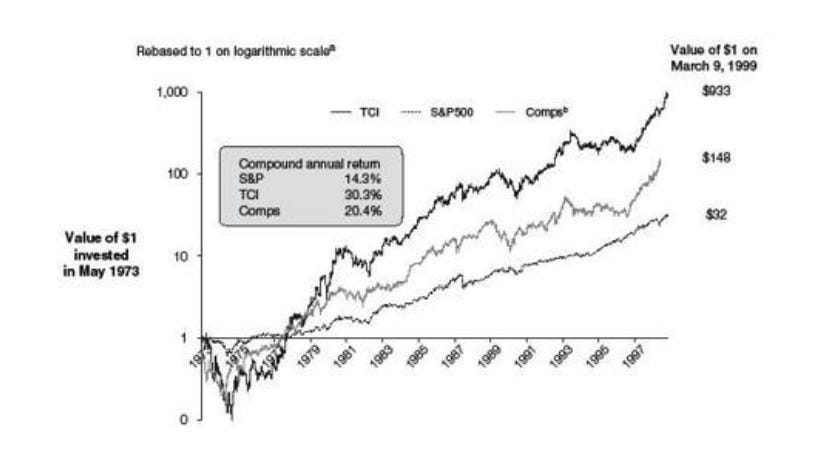

30,3% TCI vs 20,4% peers vs 14,3 S&P500

Thanks,

Finn